Article & Case Study

The Category India Can't Fund: Why No Venture-Backed Social Network

A structural analysis of why no venture-backed Indian social platform in this study has remained a profitable, standalone user-generated-content business.

This memo examines why large Indian digital marketplaces-across food delivery, quick commerce, and e-commerce, have struggled to convert scale into durable, self-sustaining value. Using a hypothesis-led analytical framework, the memo evaluates whether persistent losses and capital dependency are cyclical growing pains or the result of deeper structural constraints.

Through four sequential hypotheses, the analysis dissects supply-side stability, demand behavior, unit economics at scale, and strategic optionality. The findings suggest that platform fragility is systemic rather than transitional, with compounding frictions across supply, demand, and competition preventing normalization even at scale.

Indian digital marketplaces exhibit impressive growth in GMV, order volumes, and user reach. However, this scale has not translated into durable profitability or operating leverage.

The analysis finds that:

Platforms remain capital-dependent, with adjacencies failing to provide a credible escape path

Taken together, these dynamics trap platforms in a high-burn equilibrium, where growth increases capital requirements rather than reducing them. The issue is not execution quality or temporary competition, but a market structure that resists self-stabilization.

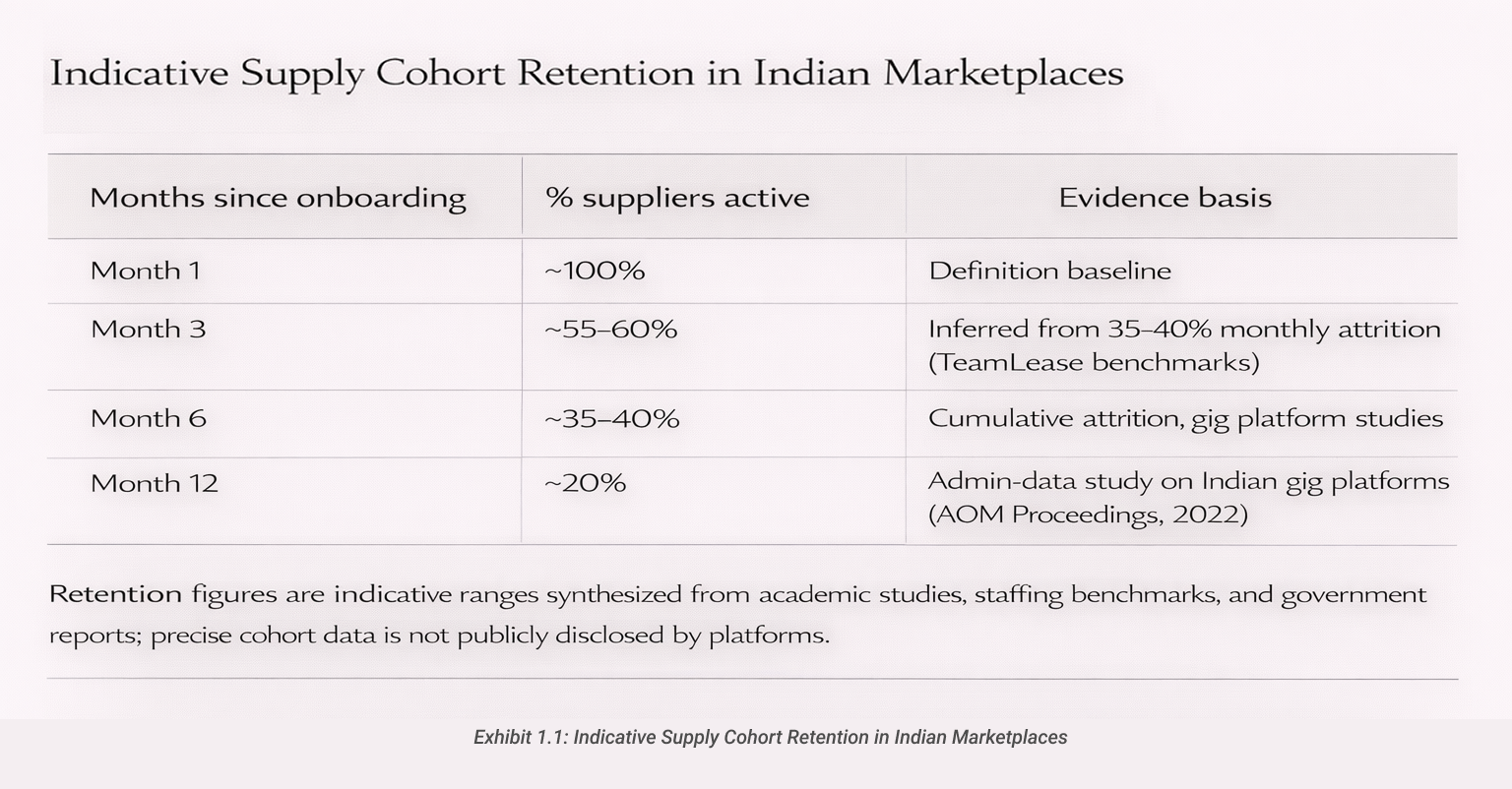

Hypothesis 1 is supported by the evidence. Indian marketplaces exhibit persistent supply-side instability driven by high churn, incentive reliance, and limited switching costs. Across delivery partners, restaurants, sellers, and gig workers, participation is economically viable primarily when supported by guarantees, bonuses, or preferential visibility. Once incentives are reduced, participation drops sharply, forcing platforms to re-subsidize supply to maintain service levels.

This fragility prevents supply from compounding with scale. Instead of benefiting from increasing density and utilization, platforms face continuous replenishment costs. High churn also undermines service consistency and increases operational overhead, limiting the ability to amortize fixed investments. As a result, scale does not meaningfully reduce cost per transaction on the supply side, weakening the foundation required for durable network effects.

(See Exhibit 1.1: Indicative Supply Cohort Retention in Indian Marketplaces)

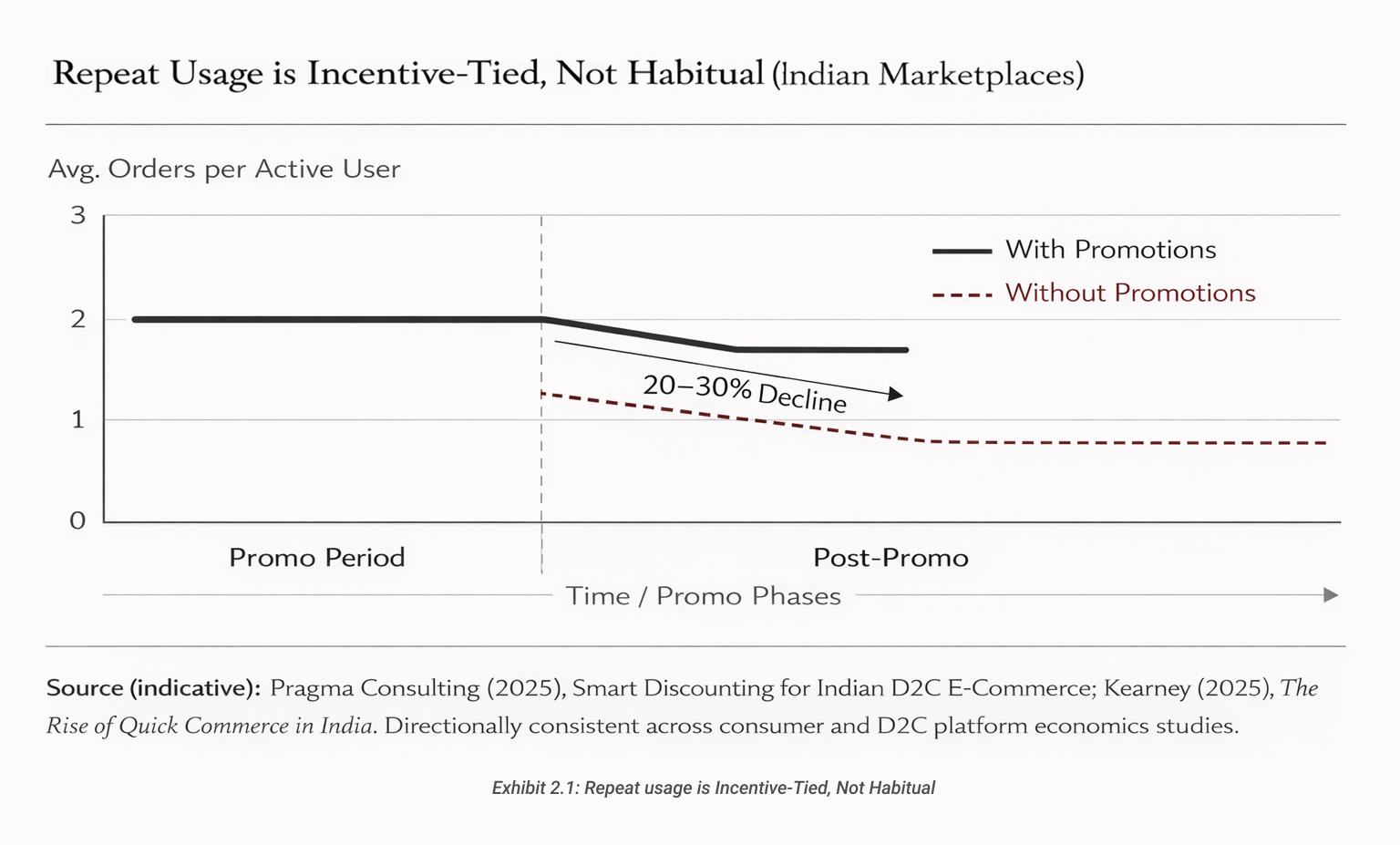

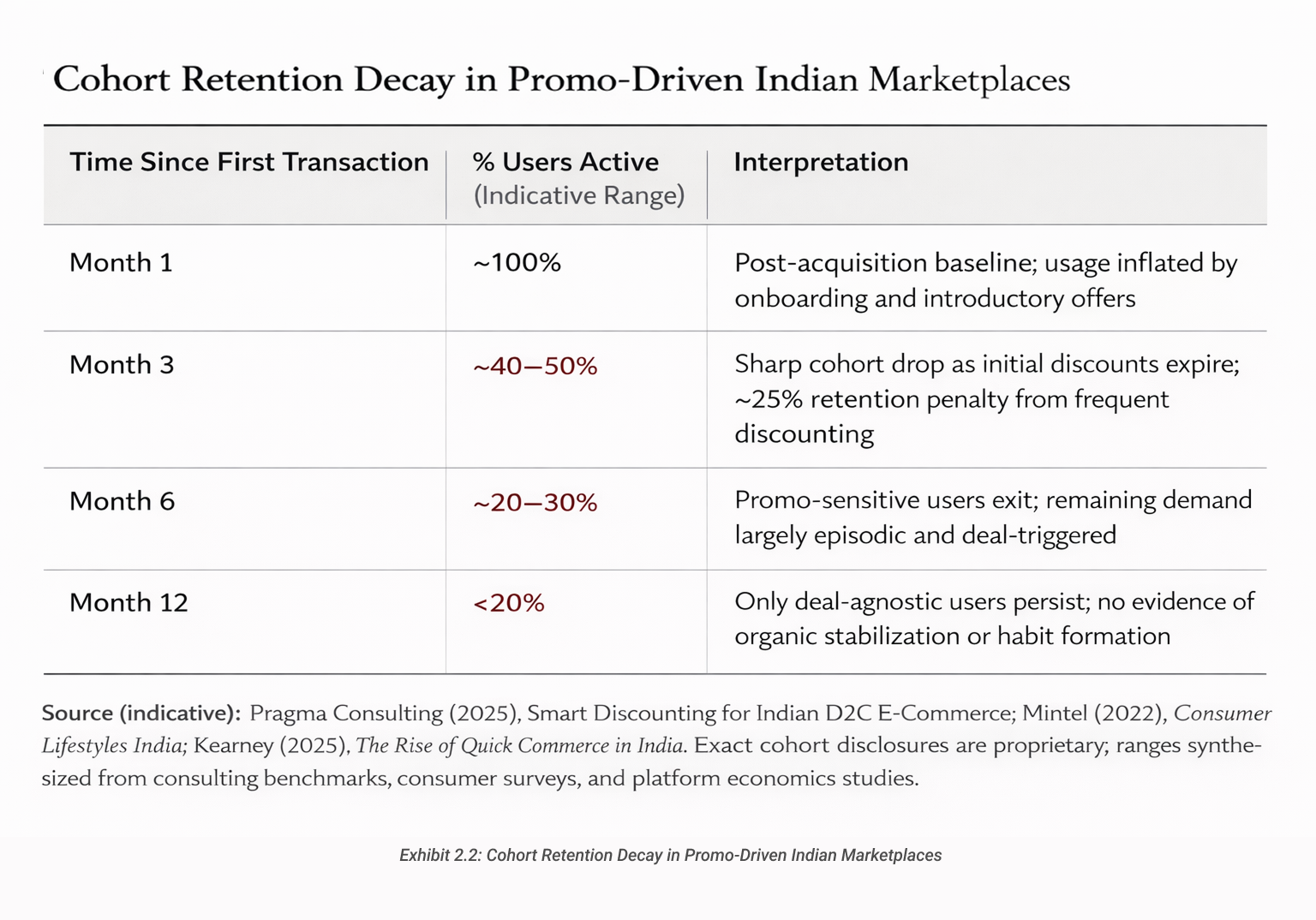

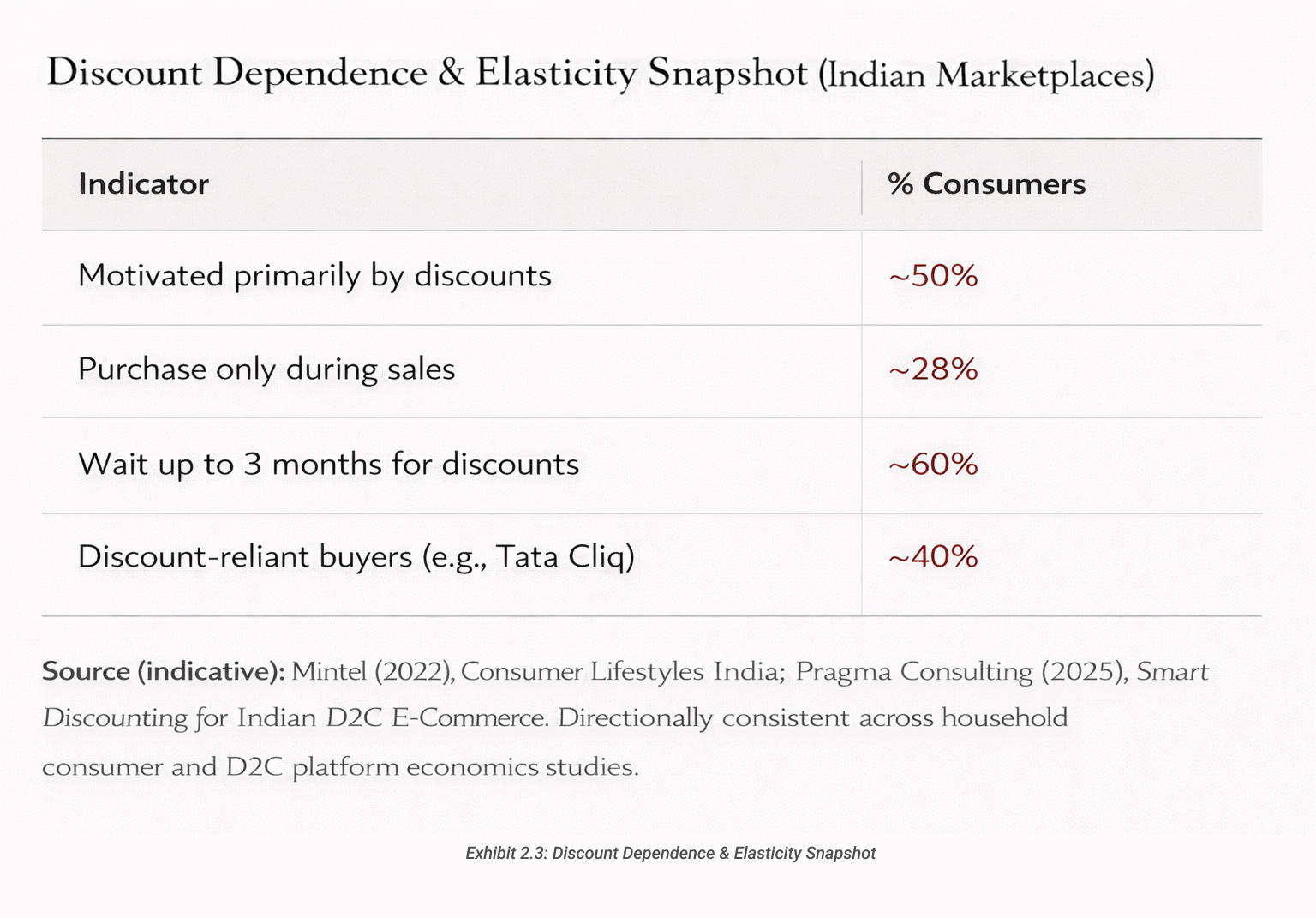

Hypothesis 2 is strongly supported by the evidence. Demand across Indian marketplaces is dominated by price sensitivity and deal-driven behavior, resulting in low repeat usage and weak loyalty. Cohort retention decays rapidly once promotions expire, with active users dropping sharply within the first few months of acquisition.

Usage intensity does not deepen with tenure: frequency and average order value remain flat or decline post-promotion, and consumers routinely multi-home across platforms to access better deals. Empirical surveys and platform benchmarks indicate that a large share of users transact only during sales or discounts, with no organic stabilization over time.

This behavior prevents platforms from converting scale into habitual usage. Instead of compounding engagement, demand resets with each incentive cycle, reinforcing dependency on continuous promotions and undermining network effects.

(See Exhibit 2.1: Repeat usage is Incentive-Tied, Not Habitual) (See Exhibit 2.2: Cohort Retention Decay in Promo-Driven Indian Marketplaces) (Se Exhibit 2.3: Discount Dependence & Elasticity Snapshot)

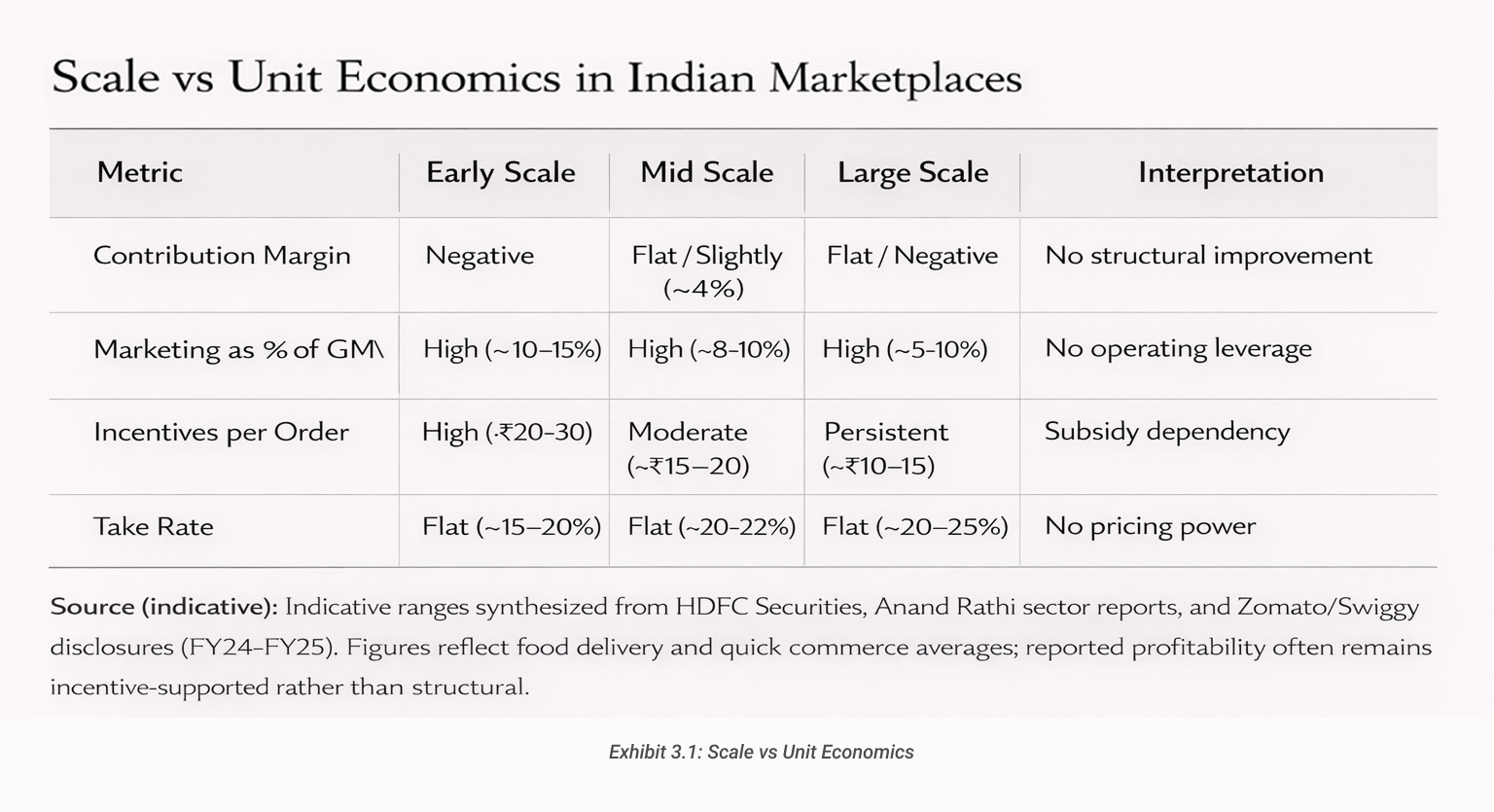

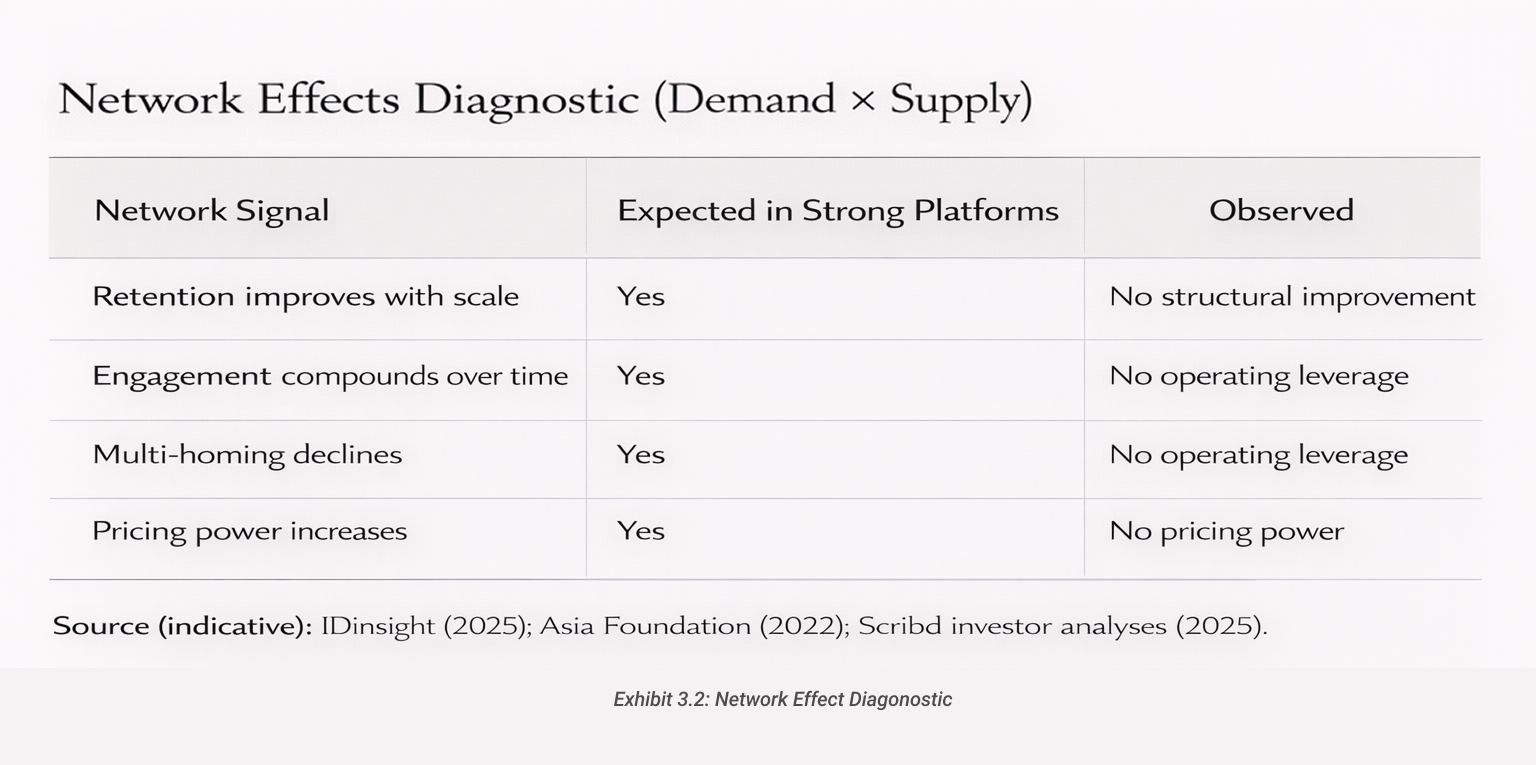

Hypothesis 3 is supported by the evidence. Despite significant growth in order volumes and GMV, Indian marketplaces have not demonstrated structural improvement in unit economics at scale. Contribution margins remain flat or marginally positive only in isolated cases, with cost per order and incentive intensity failing to decline meaningfully as platforms mature.

Marketing and subsidies continue to absorb a high share of GMV even at large scale, indicating the absence of operating leverage. Where limited profitability exists, it is typically incentive-supported and does not generalize across categories.

Moreover, scale has not produced strong or symmetric network effects. Retention and engagement do not compound in mature cohorts, multi-homing persists, and pricing power remains limited. These outcomes confirm that scale alone does not resolve the underlying supply and demand frictions identified in H1 and H2.

(See Exhibit 3.1: Scale vs Unit Economics) (See Exhibit 3.2: Network Effect Diagonostic)

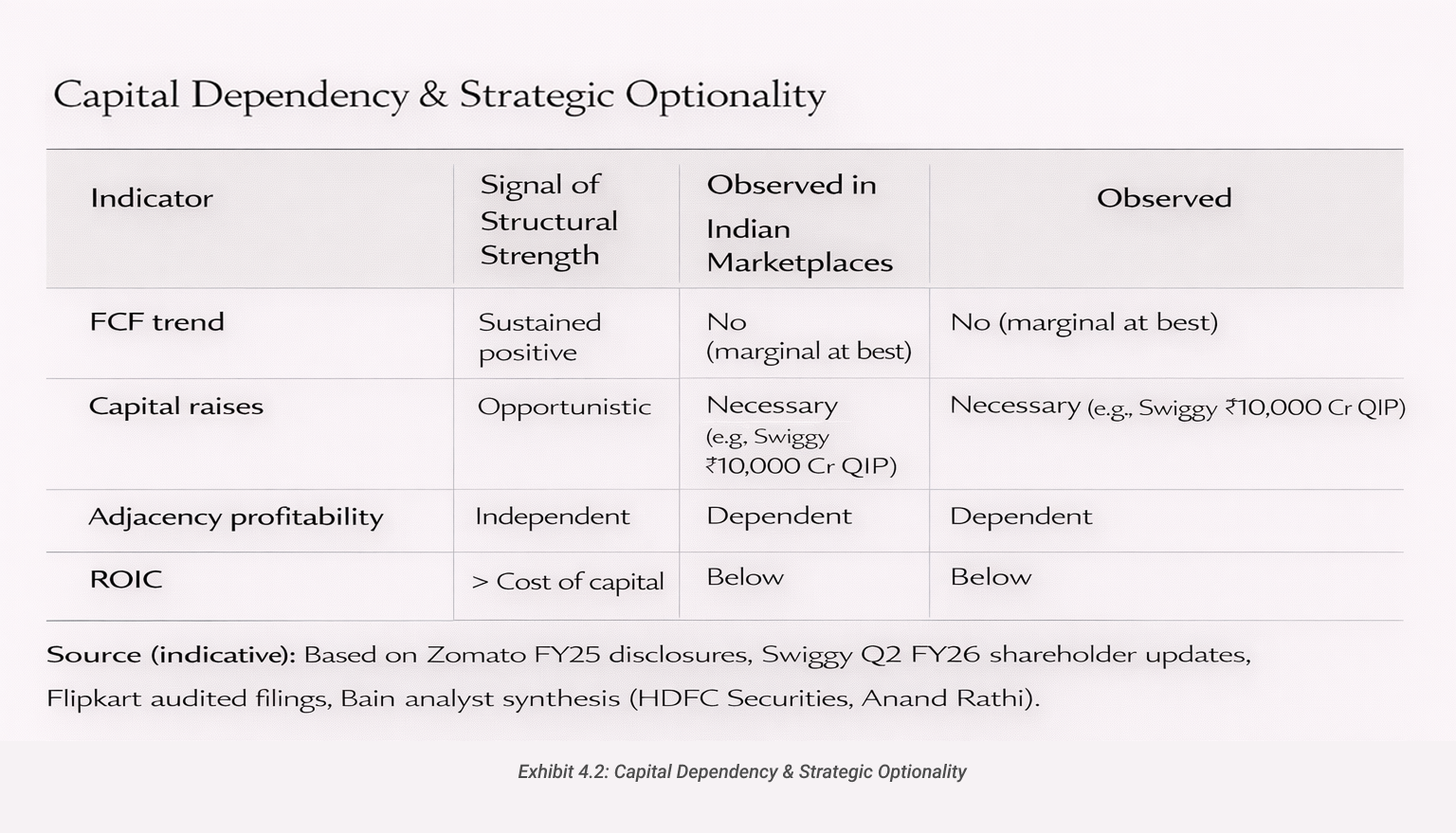

Hypothesis 4 is supported by the evidence. Despite isolated profitability in core segments, Indian marketplaces have not demonstrated a credible path to durable, internally generated value creation. Free cash flow remains negative or marginal relative to operating scale, with reported profits often masking continued reliance on external capital to fund growth and adjacencies.

New verticals - particularly quick commerce-remain subsidy-heavy and margin-dilutive, requiring incremental funding rather than offsetting core marketplace fragilities. Competitive intensity further constrains normalization: low switching costs and persistent rivalry cap pricing power, preventing sustained margin expansion even as demand grows.

Collectively, these dynamics confirm that capital raises are necessary rather than opportunistic, and that adjacencies have not emerged as independent profit engines. When combined with the fragilities identified in H1–H3, the system converges toward a high-burn equilibrium, where scale increases capital requirements rather than reducing them.

(See Exhibit 4.1: Sourse of Value Creation vs Observed Reality) (See Exhibit 4.2: Capital Dependency & Strategic Optionality)

Across all four hypotheses, a consistent pattern emerges: Indian marketplaces do not self-correct with scale. Supply churn necessitates incentives; demand responds primarily to price; scale fails to create leverage; and capital remains the binding constraint.

These forces reinforce one another. Promo-driven demand accelerates supply churn, which increases subsidy requirements, which in turn prevents margin expansion and forces further capital infusion. The result is not a temporary phase, but a structurally stable equilibrium-one that sustains growth but resists profitability.

Absent fundamental changes to market structure, pricing power, or user behavior, Indian digital marketplaces are likely to remain growth-driven but capital-intensive.

Selected references used in this analysis:

A structural analysis of why no venture-backed Indian social platform in this study has remained a profitable, standalone user-generated-content business.

This memo examines the structural conditions under which consumer internet business Actually Work in India.

This memo analyzes why many Indian consumer internet businesses fail to translate scale into sustainable profitability.

This memo examines why quick commerce scaled in India using a hypothesis-led structural analysis.

This memo examines why quick commerce scaled in India using a hypothesis-led structural analysis.