Article & Case Study

The Category India Can't Fund: Why No Venture-Backed Social Network

A structural analysis of why no venture-backed Indian social platform in this study has remained a profitable, standalone user-generated-content business.

This memo analyzes why many Indian consumer internet businesses fail to translate scale into sustainable profitability. The analysis follows a hypothesis-led, evidence-driven methodology, commonly used in management consulting and investment research.

Starting from the observed outcome-persistent losses despite scale-the memo formulates four structural hypotheses. Each hypothesis is evaluated using publicly available disclosures, consulting benchmarks, analyst commentary, and sector research. The goal is not to assess individual company execution, but to understand the underlying economic constraints shaping outcomes across categories.

Indian consumer internet platforms have demonstrated strong ability to scale users, transactions, and GMV across categories such as food delivery, quick commerce, mobility, and e-commerce. However, this scale has not consistently translated into durable unit-level profitability.

This memo finds that the challenge is structural rather than cyclical or execution-driven. Four reinforcing factors limit margin expansion at scale:

Together, these forces explain why scale improves topline metrics but fails to unlock sustained profitability across much of India’s consumer internet ecosystem.

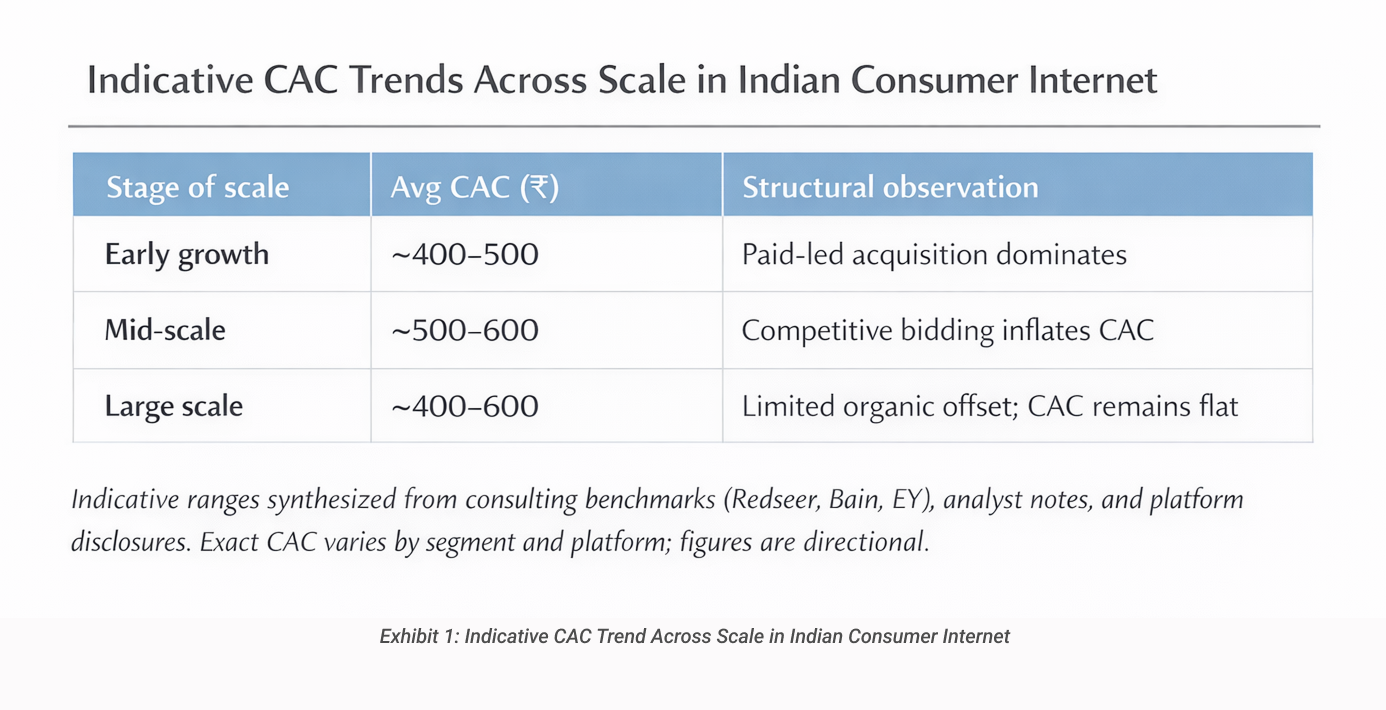

Evidence suggests that customer acquisition costs (CAC) in Indian consumer internet businesses do not decline materially as platforms scale. Unlike mature digital markets where brand strength and organic demand progressively replace paid acquisition, Indian platforms operate in highly competitive environments where multiple players bid for the same users. This competition neutralizes brand advantages and sustains paid channels as the primary growth driver even at large scale. As shown in Table H1, indicative CAC ranges remain broadly flat across growth stages, with mid- and large-scale platforms exhibiting acquisition costs comparable to early-stage levels. Consulting benchmarks and platform disclosures further indicate that marketing spend continues to scale closely with user and order growth rather than decoupling over time. As a result, scale improves topline metrics but does not structurally lower acquisition costs, constraining contribution margin expansion.

(See Exhibit 1: Indicative CAC Trend Across Scale in Indian Consumer Internet)

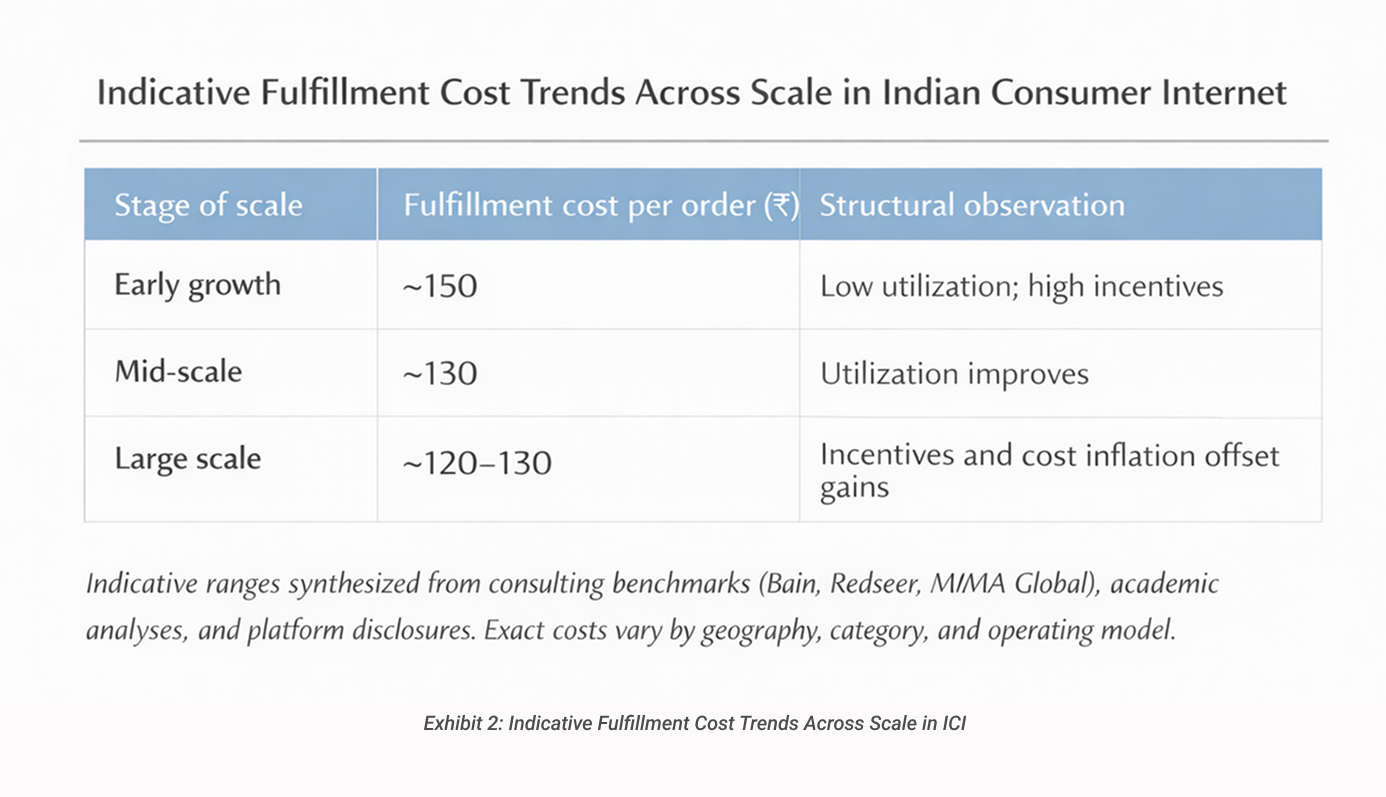

Evidence indicates that fulfillment and variable service costs in Indian consumer internet businesses remain structurally high even as platforms scale. While early growth delivers some efficiency gains through improved asset utilization and operational learning, these benefits do not compound at larger scale. Persistent incentive requirements, rising labor and fuel costs, and increasing compliance and operating complexity offset utilization-driven savings. As shown in Table H2, indicative fulfillment costs per order decline modestly during early scaling but flatten at larger scale, remaining a significant share of order value. Industry benchmarks consistently indicate that last-mile and service costs account for roughly one-third of average order value across mature platforms. This dynamic creates a structural ceiling on contribution margins, limiting the extent to which scale alone can translate into sustainable profitability.

(See Exhibit 2: Indicative Fulfillment Cost Trends Across Scale in ICI)

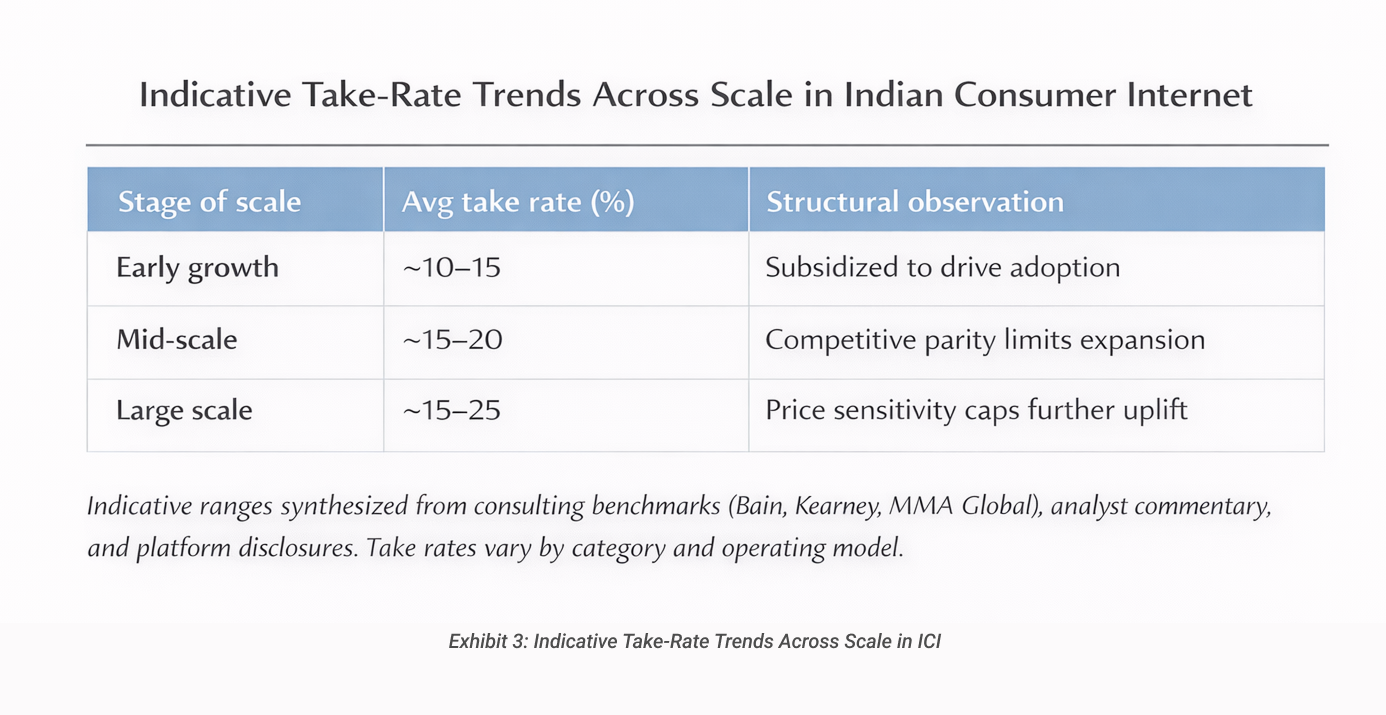

Evidence indicates that Indian consumer internet platforms face structurally limited pricing power, preventing meaningful expansion of take rates as they scale. Despite growing transaction volumes and broader platform reach, competitive parity across categories restricts the ability to raise fees without risking demand loss. As shown in Table H3, average take rates rise modestly during early growth but plateau at mid-scale levels, with little further uplift at large scale. This reflects high consumer price sensitivity, where demand responds quickly to price changes and platforms continue to rely on discounts and promotions to sustain frequency. Consequently, recent margin improvements have been driven primarily by ancillary revenue streams such as advertising and subscriptions rather than higher core transaction monetization. This dynamic limits the extent to which scale can translate into durable unit-level profitability.

(See Exhibit 3: Indicative Take-Rate Trends Across Scale in ICI)

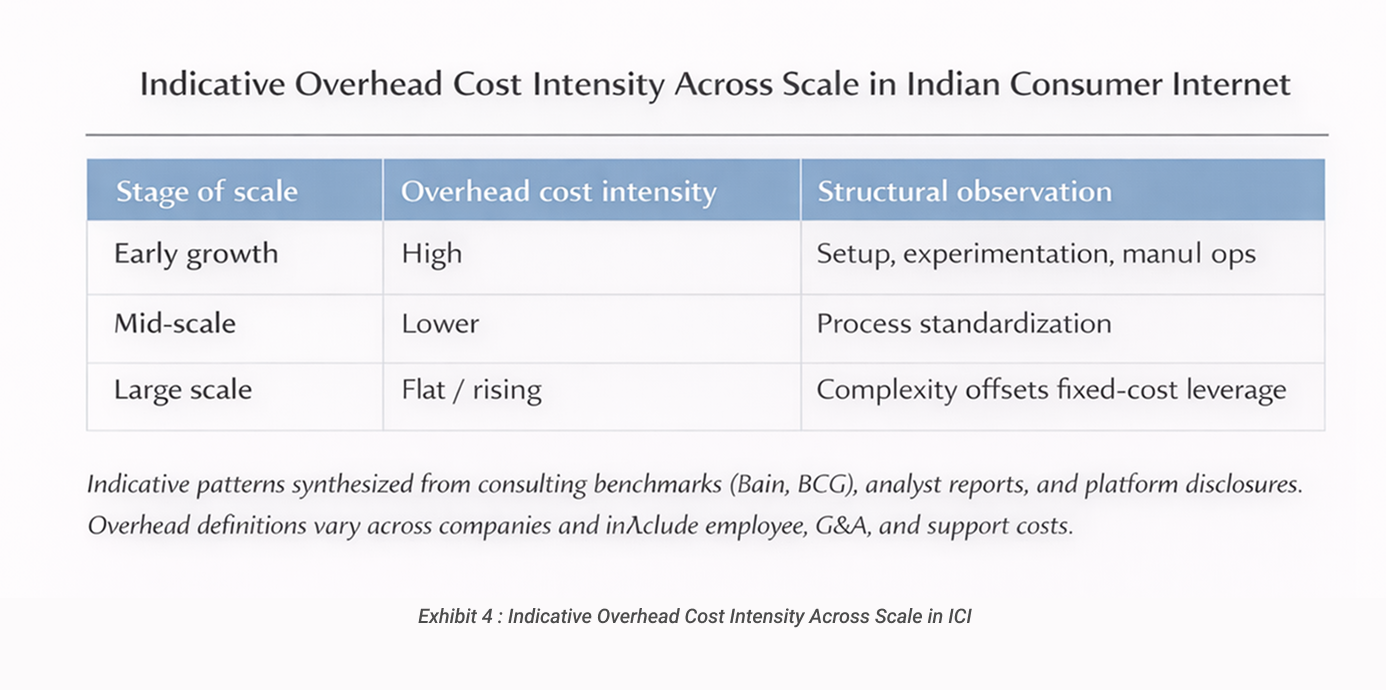

Evidence indicates that operating complexity in Indian consumer internet businesses increases with scale, delaying the realization of fixed-cost leverage. While early scaling enables some process standardization and overhead dilution, these benefits weaken as platforms expand across geographies and categories. India’s fragmented markets require localized operations, additional control layers, and expanded support functions, causing overhead costs to remain flat or rise at larger scale. As shown in Table H4, overhead intensity does not decline cleanly beyond mid-scale, reflecting the growing burden of organizational, compliance, and operational complexity. Platform disclosures and industry benchmarks further suggest that headcount and support functions continue to scale closely with transaction volumes. As a result, operating leverage emerges slowly and inconsistently, preventing scale from translating into stable, platform-wide profitability.

(See Exhibit 4: Indicative Overhead Cost Intensity Across Scale in ICI)

Taken together, the four hypotheses explain a consistent pattern across Indian consumer internet platforms. Scale does deliver volume growth, but it does not reliably unlock economic self-reinforcement. Acquisition costs remain high, variable costs do not compress, pricing power is constrained, and overhead complexity rises with expansion. Rather than compounding, scale exposes structural frictions that delay or neutralize operating leverage. Profitability, where it appears, is often driven by ancillary revenues or model pivots rather than core unit-level improvement.

The challenge facing Indian consumer internet businesses is not an absence of scale, ambition, or execution capability. It is a structural mismatch between the economics required for digital platform profitability and the realities of India’s competitive, price-sensitive, and operationally complex markets. Until these structural constraints ease-or business models adapt to work around them-scale alone is unlikely to be sufficient for sustained profitability.

The analysis draws on public disclosures, consulting research, and analyst commentary, including:

A structural analysis of why no venture-backed Indian social platform in this study has remained a profitable, standalone user-generated-content business.

This memo examines the structural conditions under which consumer internet business Actually Work in India.

A hypothesis-led systems analysis of food delivery, quick commerce, and e-commerce platforms.

This memo examines why quick commerce scaled in India using a hypothesis-led structural analysis.

This memo examines why quick commerce scaled in India using a hypothesis-led structural analysis.