Article & Case Study

The Category India Can't Fund: Why No Venture-Backed Social Network

A structural analysis of why no venture-backed Indian social platform in this study has remained a profitable, standalone user-generated-content business.

This memo examines why quick commerce has scaled in India, using a hypothesis-led analysis across market structure, demand behavior, fulfillment design, and ecosystem leverage.

Quick commerce in India has defied early skepticism around unit economics, scalability, and consumer behavior. While the model remains structurally constrained outside dense urban markets, evidence suggests that its relative success in India is not accidental but the result of a convergence of market structure, demand evolution, operating design, and ecosystem support.

This memo examines four hypotheses to explain why quick commerce has scaled in India:

Taken together, these factors explain not only where and why quick commerce works today-but also why it survived long enough to reach its current scale.

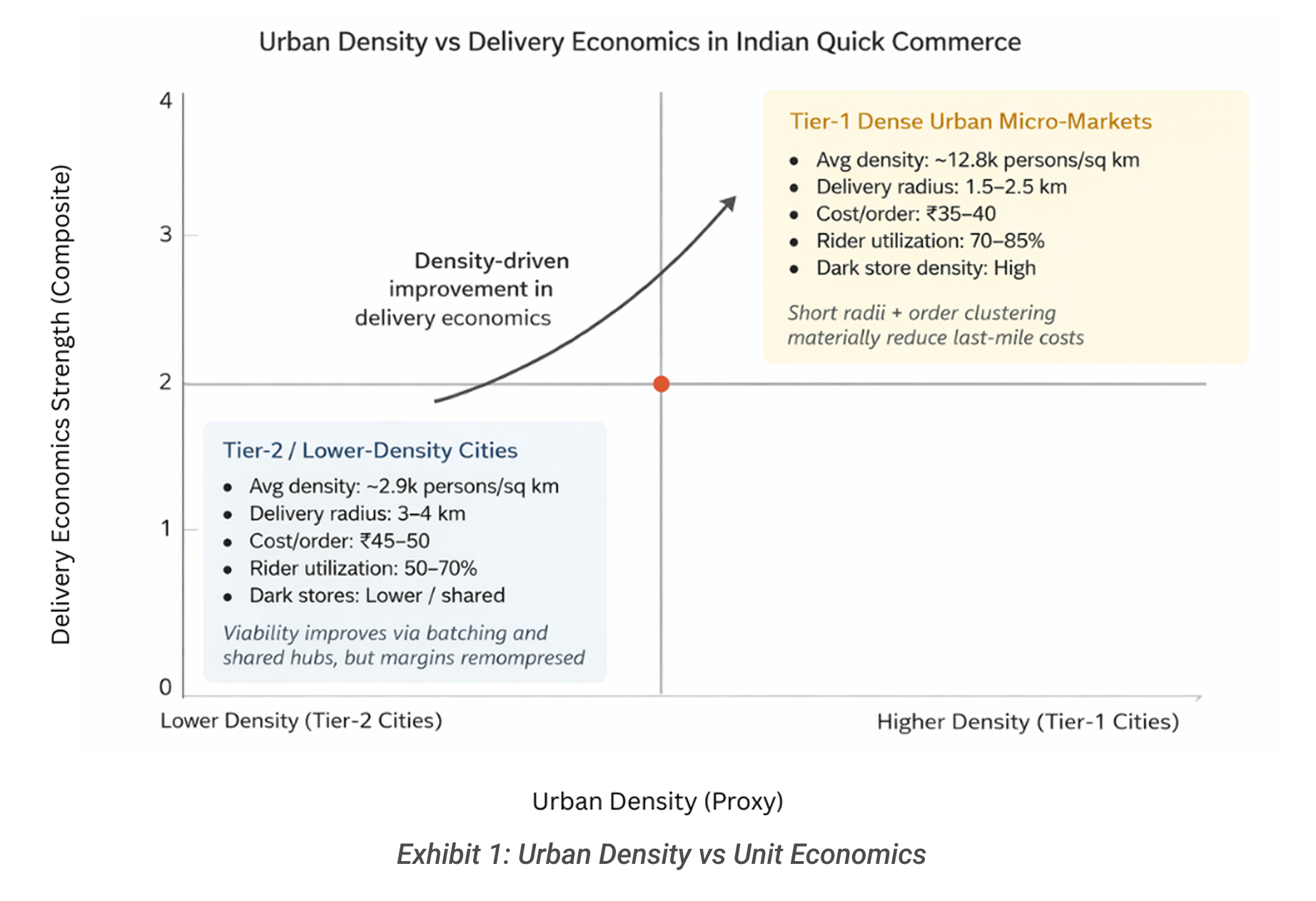

Quick commerce unit economics are structurally strongest in high-density urban micro-markets, where short delivery radii and order clustering materially reduce last-mile costs. Across Tier-1 cities, dense neighborhoods support:

Implication: Quick commerce is not a nationwide model-it is a micro-market model, economically viable only where urban density supports high throughput.

(See Exhibit 1: Urban Density vs Unit Economics)

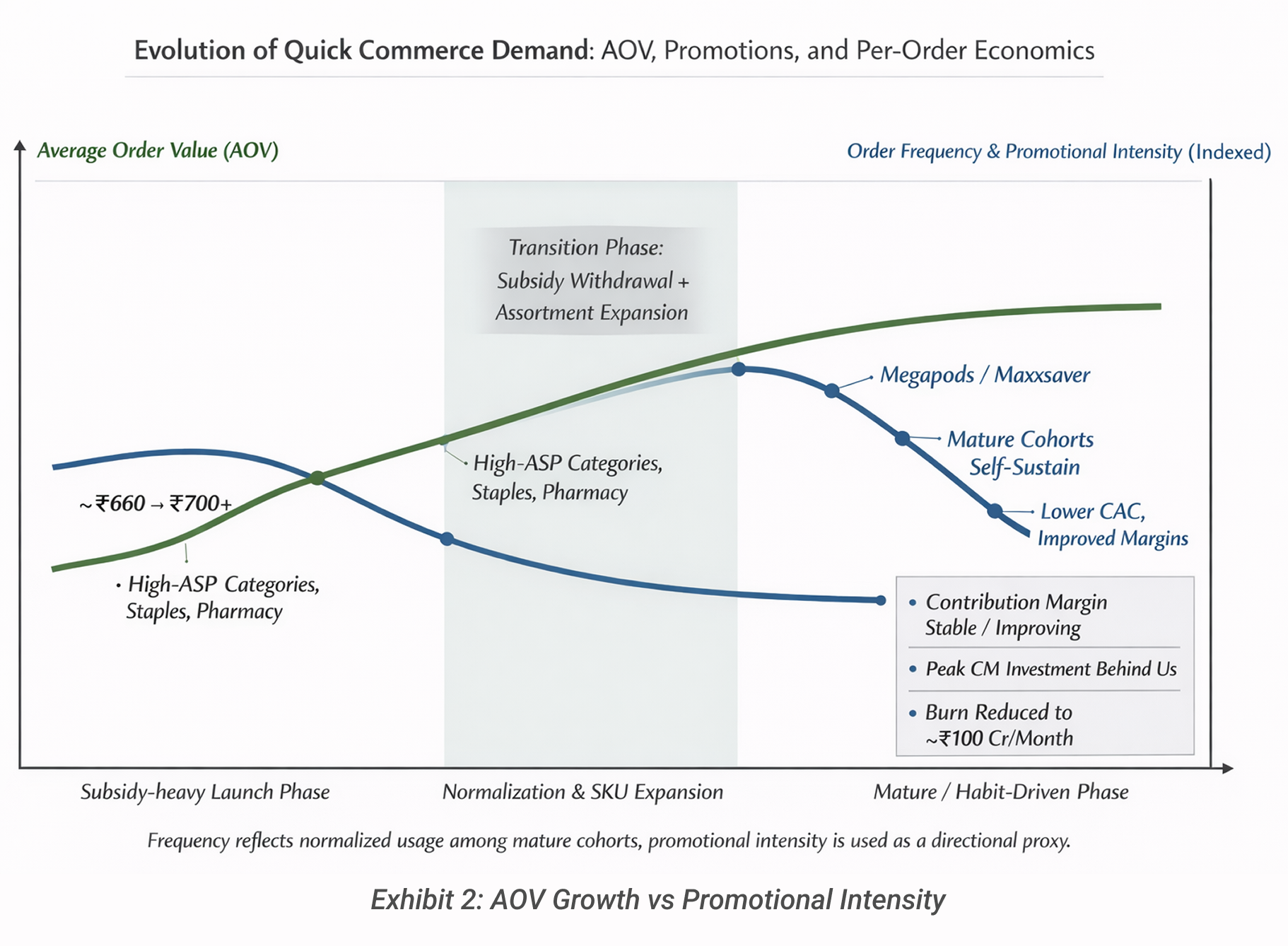

Early quick commerce demand was heavily subsidy-driven, characterized by small, impulsive orders. Over time, management commentary and operational metrics indicate a shift toward higher AOV baskets, driven by:

Implication: Quick commerce demand has matured, trading frequency for value-improving per-order economics even as growth normalizes. (See Exhibit 2: AOV Growth vs Promotional Intensity)

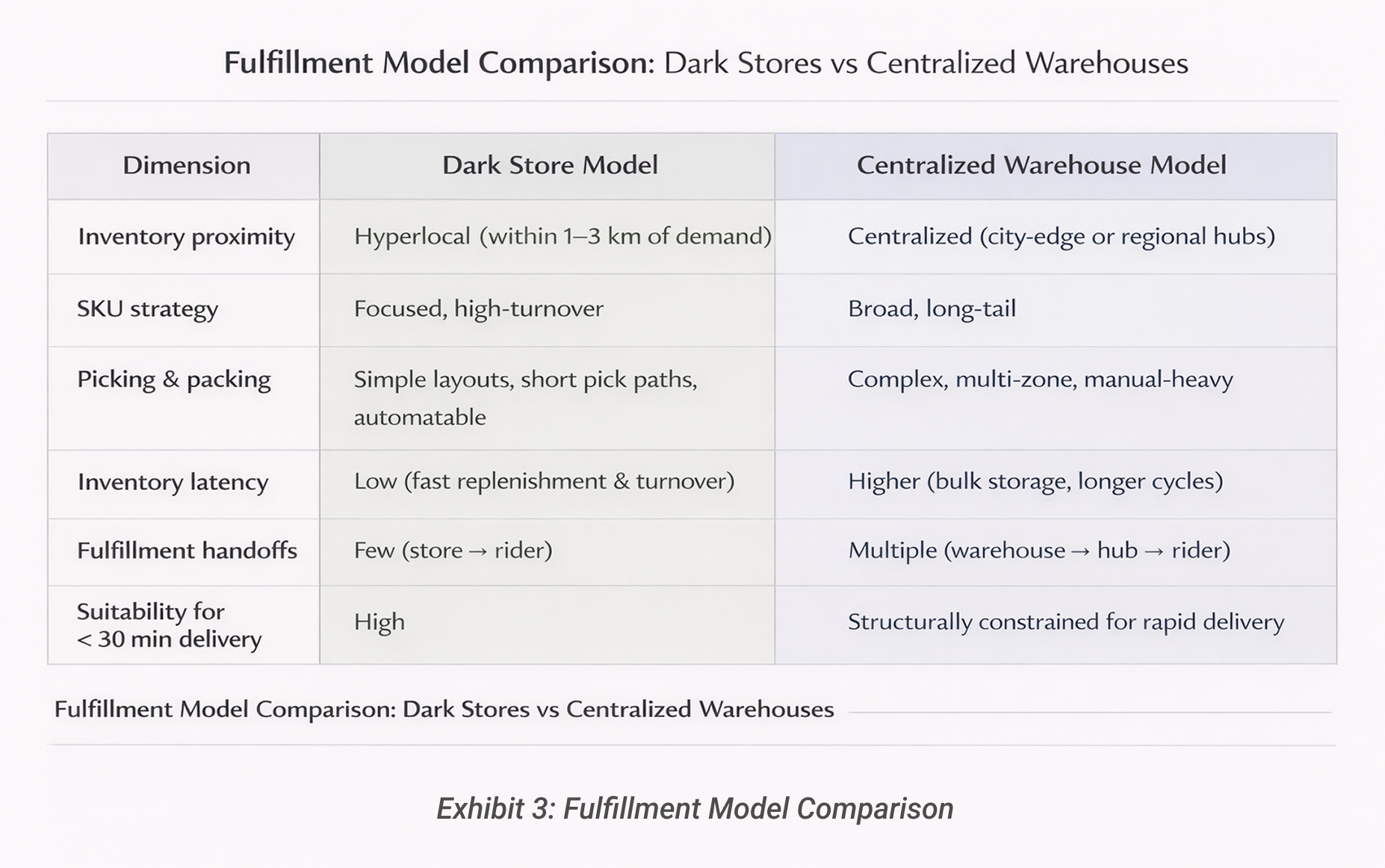

Quick commerce economics align more closely with dark-store–based fulfillment than with centralized warehouse models. Dark stores:

Implication: Quick commerce success depends less on execution excellence and more on structural fit between demand speed and fulfillment design. (See Exhibit 3: Fulfillment Model Comparison)

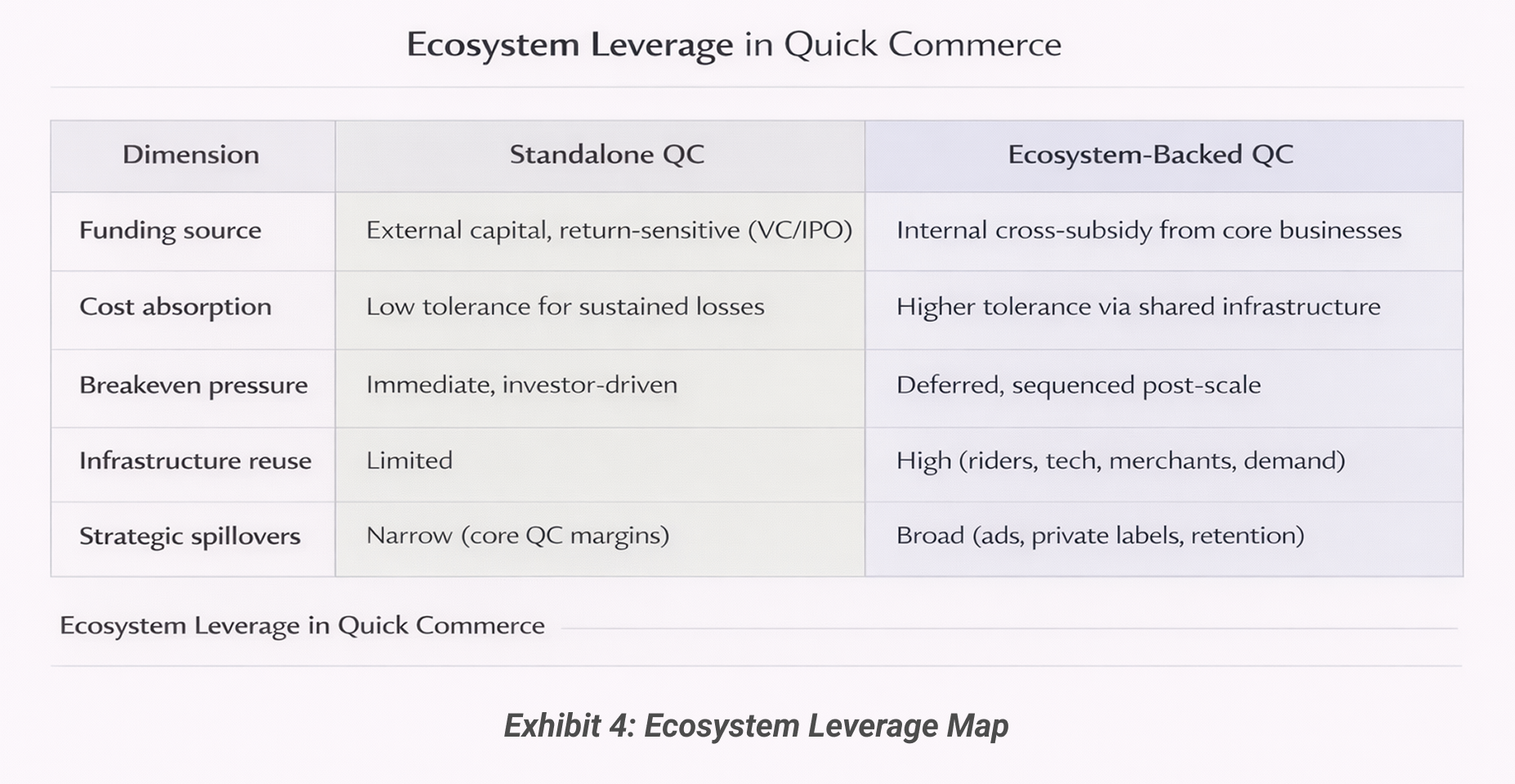

Quick commerce viability in India has been reinforced by ecosystem backing, particularly among integrated platforms. Ecosystem-backed models benefit from:

Implication: Quick commerce did not succeed despite losses - it survived because ecosystems could absorb them long enough for structural advantages to emerge. (See Exhibit 4: Ecosystem Leverage Map)

Quick commerce works in India conditionally, not universally. It succeeds when:

Selected references used in this analysis:

A structural analysis of why no venture-backed Indian social platform in this study has remained a profitable, standalone user-generated-content business.

This memo examines the structural conditions under which consumer internet business Actually Work in India.

This memo analyzes why many Indian consumer internet businesses fail to translate scale into sustainable profitability.

A hypothesis-led systems analysis of food delivery, quick commerce, and e-commerce platforms.

This memo examines why quick commerce scaled in India using a hypothesis-led structural analysis.